Fintech Unicorn Moneyview Files DRHP for ₹1,500 Crore IPO: A Deep Dive into the Lending Giant’s Journey

Fintech unicorn Moneyview files DRHP with SEBI for a ₹1,500 crore IPO. Discover the company’s journey from an expense tracker to a lending giant, its financial growth, and IPO details.

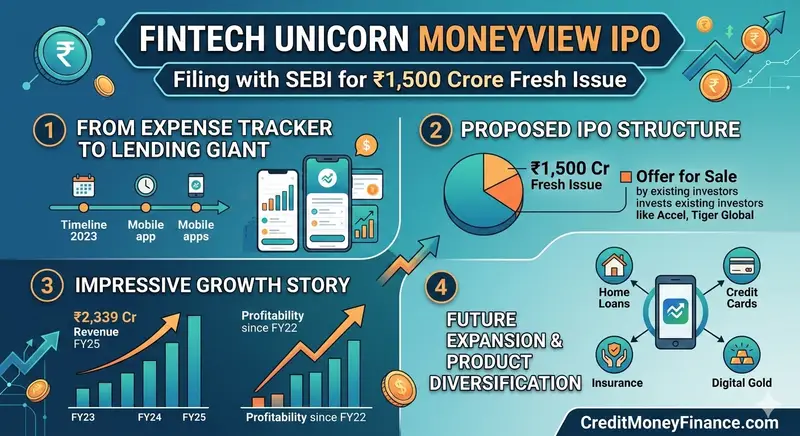

The Indian fintech landscape is witnessing another landmark moment as Moneyview, the Bengaluru-based digital lending unicorn, has officially filed its Draft Red Herring Prospectus (DRHP) with the Securities and Exchange Board of India (SEBI). Seeking to raise ₹1,500 crore through a fresh issue, the company is eyeing a public debut that underscores the massive growth of digital credit in “Middle India.”

The Genesis: From Expense Tracking to a Lending Powerhouse

Founded in 2014 by IIT Delhi alumni Puneet Agarwal and Sanjay Aggarwal, Moneyview didn’t start as a lender. Its journey began as a Personal Financial Management (PFM) app designed to help users track their spending via SMS alerts.

However, the founders soon identified a significant gap: millions of creditworthy Indians were being ignored by traditional banks due to a lack of formal credit scores. In 2016, the company pivoted to digital lending, leveraging an AI-powered risk engine that analyzes alternative data points to provide credit to the “credit invisible” segments.

The IPO Breakdown: Where Will the Money Go?

The proposed Initial Public Offering (IPO) is a strategic mix of capital infusion and an exit path for early backers.

1. Issue Structure

- Fresh Issue: Up to ₹1,500 crore.

- Offer for Sale (OFS): Approximately 13.6 crore equity shares by existing shareholders and promoters.

- Face Value: ₹1 per equity share.

2. Utilization of Funds

According to the DRHP, Moneyview has a clear roadmap for the ₹1,500 crore fresh capital:

- ₹650 crore: To scale loan disbursals under Default Loss Guarantee (DLG) arrangements.

- ₹450 crore: To augment the capital base of its subsidiary NBFC, Whizdm Finance Private Limited.

- Balance: Reserved for general corporate purposes and strategic inorganic growth.

Financial Performance: A Trajectory of Profitability

Unlike many late-stage startups that struggle with “burn,” Moneyview has maintained a track record of profitability since FY22.

|

Metric |

FY24 |

FY25 |

Growth (YoY) |

|---|---|---|---|

|

Operating Revenue |

₹1,342.37 Cr |

₹2,339.15 Cr |

~74% |

|

Net Profit (PAT) |

₹171.15 Cr |

₹240.28 Cr |

~40% |

|

Managed AUM |

– |

₹19,814 Cr* |

– |

*AUM figure as of December 31, 2025.

The company’s efficiency is further highlighted by its operating leverage. Operating expenses as a percentage of total income plummeted from 62.84% in FY23 to just 35.19% by late 2025, signaling a highly scalable tech-first model.

Investor Confidence and Unicorn Status

Moneyview reached the coveted Unicorn status in 2024 after a series of successful funding rounds. The company has raised over $230 million to date from marquee global investors.

Key Shareholders (Pre-IPO):

- Accel India: 21.31%

- Tiger Global (Internet Fund III): 13.79%

- Ribbit Capital: 10.20%

- Apis Growth: 6.61%

Other notable investors include Evolvence India, Winter Capital, and Nexus Venture Partners.

Future Growth Potential: Beyond Personal Loans

While digital personal loans remain the flagship product, Moneyview is evolving into a full-stack financial services platform. Its growth strategy focuses on:

- Product Diversification: Scaling newer offerings like Home Loans, Loans Against Property (LAP), and Credit Cards.

- Expanding Reach: Currently serving 125 million+ users across 99.55% of India’s PIN codes, with 79% of customers residing in Tier 2+ cities.

- Cross-selling: Utilizing its massive user base to offer Insurance, Digital Gold, and Earned Wage Access.

Conclusion for Investors

Moneyview’s IPO comes at a time when the Indian markets are rewarding profitable, high-growth fintech firms. With a Managed AUM of nearly ₹20,000 crore and a robust AI risk engine, the company stands out as a dominant player in the unsecured lending space. For retail investors, the key will be the valuation at which the company ultimately hits the market.

Team: YuvaMorcha.com

More Featured Articles:

SME IPOs in India: Insights from Regulators, Bankers & Advisors

How Ex-Bankers Can Build a High-Income Second Career Through a Corporate DSA Partner Program

India’s REITs Surge as SEBI Reclassification Boosts Investor Confidence

Top 10 Angel Investment Networks in India (2026): The Ultimate Founder’s Guide to Fundraising.

SIDBI – Powering India’s MSME Growth: Funding, Schemes & Business Support.

IIT Bombay Launches First-of-Its-Kind ₹250 Crore Deep-Tech VC Fund to Empower Early-Stage Startups

CFO Services for Startups: Why Virtual CFOs are Becoming a Game-Changer in India

The Ultimate Guide to Collateral-Free Business Finance: Scaling Beyond Physical Assets.